Ever wondered how businesses keep their shipped goods safe during long journeys? Enter cargo insurance – a superhero for your packages! Cargo insurance is like a superhero cape, protecting stuff from getting hurt or lost on the way.

In this guide, we’ll chat about what cargo insurance is, its different types, and why it’s a big deal. Imagine it as a special shield for your things, making sure they arrive safe and sound, no matter how far they travel. From unraveling the types of coverage to figuring out why businesses love it, let’s make cargo insurance as easy as pie. Get ready to become a shipping superhero and keep your goods smiling from start to finish!

What is Cargo Insurance?

Cargo insurance is a type of insurance that provides coverage for loss or damage to goods and merchandise during transportation. It is designed to protect the financial interests of the parties involved in the shipping process, including the shipper, the carrier, and the consignee. The coverage typically applies to various modes of transportation, such as sea, air, road, and rail.

Cargo insurance is essential because the transportation of goods involves various risks, including accidents, theft, natural disasters, and other unforeseen events. Without insurance, parties involved in the shipping process may face financial losses if the goods are damaged or lost during transit.

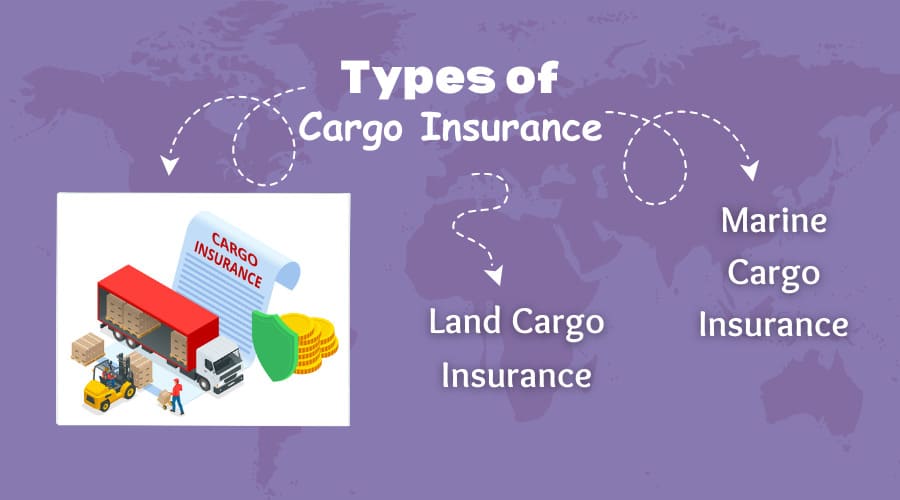

Types of Cargo Insurance: Navigating the Seas and Roads

Cargo insurance comes in two primary types: Marine Cargo Insurance and Land Cargo Insurance, each tailored to specific modes of transportation.

1. Land Cargo Insurance

Coverage Scope: Designed for cargo transported within a country’s boundaries using roads, typically in trucks or utility vehicles.

Covered Risks: Protects against collision damages, theft, and various risks associated with freight shipping on land.

Geographical Limit: Applicable to shipments within the country.

2. Marine Cargo Insurance

Coverage Scope: Geared towards international shipments via sea routes, and also covers the air portion if it’s part of the same journey.

Covered Risks: Provides coverage for damages due to bad weather conditions, loading/unloading, piracy, and other potential losses during the possession of the airline or shipping line.

Applicability: Primarily used for shipments involving sea routes and international trade.

Types of Marine Cargo Insurance Policies:

a. Single Coverage

Description: Offers coverage on a per-shipment basis.

Suitability: Ideal for small businesses or infrequent shippers.

b. Contingency Policies

Description: Places liability on the consumer to bear cargo insurance costs.

Usage: Often involves legal procedures, additional charges, and time-consuming processes.

c. Open Coverage

Description: Suitable for businesses with frequent shipments through airlines or shipping lines.

Types: Permanent (for a specific period) and Renewable (allows renewals during cargo delivery).

Types of Marine Cargo Insurance Coverage Policies:

d. Free from Particular Average

Alternative Name: Named Peril Policy.

Coverage:* Addresses major damages not covered by an all-risk policy, including force majeure events, rough weather, theft, piracy, collision, sinking, and non-delivery.

e. All-Risk Coverage Policy

Description: Covers a wide array of damages caused by external factors, but excludes certain situations like customs rejection, force majeure events, and negligence on the part of the exporter or importer.

f. General Average

Significance: Essential for marine freight.

Principle: Requires owners of surviving cargo to share the cost of loss or damage if some goods belonging to other owners are affected during transit.

Understanding these types and policies empowers businesses to choose cargo insurance that aligns with their specific transportation needs, offering tailored protection against a variety of risks.

How Cargo Insurance Works?

Understanding how Cargo Insurance works ensures a smoother process, from coverage initiation to claim resolution, in the realm of cargo insurance.

Coverage Basis:

Cargo insurance serves as protection against potential damage or loss during the transportation of goods. The policy clearly defines the incidents it covers, including theft, accidents, or natural disasters.

Premium Payment:

Securing coverage involves the upfront payment of a premium by the policyholder. This premium is typically integrated into the overall shipping fees, simplifying the process.

Claim Process:

In the event of damage or loss, the policyholder can initiate a claim. A claim adjuster meticulously assesses the claim to ensure it aligns with the specified clauses in the policy.

Claim Requirements:

When filing a claim, specific information is essential:

- Detailed item description (including size, weight, and visual indicators).

- Inventory number.

- Severity of damage.

- Age of the item and its purchase date.

- Packaging location.

- Original cost and replacement cost.

Settlement:

Valid claims result in the policyholder receiving a settlement check. The settlement amount is determined by the insured limit specified in the policy.

Claim Amount Clarification:

Clarity is key when specifying claim amounts:

- Specify repair costs for damaged goods.

- Specify the actual cost for items completely lost.

7 Key Advantages of Cargo Insurance

Here are the 7 key advantages of Cargo Insurance:

Financial Protection: Cargo insurance shields businesses from financial losses due to damage or loss of shipments during transportation, providing a safety net for unexpected events.

Comprehensive Coverage: Offers a wide range of coverage options, including protection against theft, accidents, natural disasters, and other unforeseen incidents during transit via road, sea, or air.

Risk Mitigation: Mitigates the inherent risks associated with shipping by covering potential damages, helping businesses navigate the uncertainties of the supply chain.

Peace of Mind: Provides peace of mind to shippers, ensuring they can focus on their core business activities without constant worry about the safety of their goods in transit.

Facilitates International Trade: Essential for businesses engaged in international trade, as it minimizes the financial impact of unforeseen events, fostering smoother cross-border transactions.

Customizable Policies: Cargo insurance policies are often customizable to meet the specific needs and nature of the shipped goods, allowing businesses to tailor coverage based on their unique requirements.

Claims Settlement: Simplifies the claims process, ensuring that legitimate claims are processed efficiently and that businesses receive timely settlements, helping them recover quickly from any losses incurred during transit.

What Freight & Cargo Insurance Covers

Freight and cargo insurance play a crucial role in protecting businesses from significant financial losses caused by unexpected incidents during transportation. Here are the primary coverages provided by cargo insurance companies:

Damage from Various Causes: Protection against damage caused by events like explosions, fires, or sinking during transit, whether by road, sea, or air.

Road Incidents: Coverage for additional expenses resulting from incidents like overturning, collision, or other road inconveniences.

Natural Disasters: Insurance coverage for damages caused by natural disasters such as earthquakes, floods, tsunamis, or volcanic eruptions.

Loading and Unloading:Protection in the event of package loss during loading, unloading, and handling processes.

Seawater Damage: Coverage for damages caused by the entry of seawater into ships and vessels during transportation.

In addition to the scenarios mentioned, cargo insurance companies offer varying degrees of security for shipments in other cases. Understanding these coverages is vital for businesses seeking comprehensive protection for their goods in transit.

What Freight & Cargo Insurance Excludes

While freight and cargo insurance provide crucial coverage, it’s essential to understand what they do not cover. These exclusions are typically outlined in the policy to prevent fraudulent claims and manage expectations. Here are common scenarios not covered by cargo insurance:

Inadequate Packaging: Damages resulting from improper packaging are not covered. Shipping companies often provide guidelines for packaging, especially for fragile or specific goods based on weight and volume.

Mode of Transportation Restrictions: Some policies may restrict coverage to specific modes of transportation, such as ships, large vehicles, or airplanes. Businesses should carefully review the policy to know which modes are covered.

Faulty Product Shipment: Damages caused by shipping goods with identified faults or defects are typically excluded from coverage.

Exclusion of Specific Shipments: Certain insurance companies may exclude coverage for fragile or hazardous goods. Items like electronics, metal products, or highly valuable goods may not be covered.

It’s important to note that air and marine cargo insurance adhere to the Institute of Cargo Clauses specifications. These clauses define coverage for constructive total and actual total loss, general average, liability due to collision, partial loss, and more. Businesses should thoroughly review and understand these clauses to ensure clarity on coverage limitations.”

How Much Does Cargo Insurance Cost?

Cargo insurance costs typically amount to around 0.15% of the total value of goods, as indicated on the commercial invoice. However, it’s crucial to note that this percentage can vary among different insurance providers and their specific policies.

The commercial invoice serves as a key reference point for determining the insurance premium, ensuring that the coverage aligns with the declared value of the shipped goods. Various factors, including the nature of the goods, mode of transportation, and the level of coverage required, can influence the final cost of cargo insurance.

Businesses are advised to carefully review and compare insurance offerings to select a policy that not only suits their budget but also provides adequate coverage for the potential risks associated with the transportation of goods.

The calculation of cargo insurance follows a standard CIF+10% formula. This method involves three key components:

Commercial Invoice Value (C): Consider the selling cost if you’re the seller or the purchase cost if you’re the buyer.

Insurance Premium (I): This is the cost of insuring the shipment against potential risks.

Freight and Associated Charges (F): Includes expenses like customs clearance charges and other relevant freight costs.

To factor in the impact of inflation in freight costs, add 10% to the total of these components. The resulting sum is the CIF (Cost, Insurance, Freight) value of the shipment. For example, if the Commercial Invoice Value is USD 60,000, the Insurance is USD 300, and the shipping charge is USD 1,000, then the CIF value is USD 61,300.

In the final step, apply the insurance rate provided by the insurance company to calculate the total insurance payable. This straightforward formula ensures a clear understanding of the insurance cost for a given shipment.

Difference Between Cargo and Freight Insurance?

Cargo insurance and freight insurance are terms often used interchangeably, but they refer to distinct aspects within the realm of shipping and transportation.

Here are the key differences between cargo and freight insurance:

Coverage Focus:

Cargo Insurance: Primarily focuses on protecting the goods or merchandise being transported from loss or damage during transit. It is concerned with the physical integrity of the shipped items.

Freight Insurance: Encompasses a broader scope, covering financial losses related to the entire shipping process. This includes not only the goods but also the freight charges, ensuring coverage for the financial investment in the entire shipment.

Nature of Coverage:

Cargo Insurance: Specifically addresses the value of the goods being transported and the potential loss or damage to those goods during the journey.

Freight Insurance: Extends coverage beyond the goods themselves to include the costs associated with shipping, such as freight charges and other relevant expenses.

Parties Covered:

Cargo Insurance: Primarily benefits the owner of the goods or the party with a financial interest in the shipped items.

Freight Insurance: Offers protection to various parties involved in the transportation process, including the shipper, carrier, and consignee, safeguarding their financial interests throughout the shipping journey.

Insurance Premium Determinants:

Cargo Insurance: The premium is calculated based on the value of the goods being shipped.

Freight Insurance: Considers a broader range of factors, including the value of goods, freight charges, and other associated costs, influencing the overall premium.

Conclusion: Safeguarding Shipments, Empowering Businesses

In the intricate world of global trade and logistics, cargo insurance emerges as a crucial ally, ensuring the safe passage of goods and bolstering the resilience of businesses against unforeseen challenges. Whether navigating the seas or roads, understanding the nuances of cargo and freight insurance becomes paramount for businesses seeking comprehensive protection.

From the superhero-like coverage provided by cargo insurance to the nuanced differences between land and marine policies, this guide has unraveled the complexities, offering businesses a compass for securing their shipments. The advantages of cargo insurance, cost considerations, and the calculation intricacies have been demystified, empowering businesses to make informed decisions tailored to their unique needs.

As businesses embark on their shipping endeavors, armed with the knowledge encapsulated in this guide, they can confidently navigate the seas of international trade, ensuring their goods arrive unscathed and their financial interests remain fortified. Cargo insurance is not merely a protective shield; it’s a strategic tool that propels businesses forward with confidence, turning each shipment into a success story.

Also Read : Why is Export Factoring Important to Your Business?