In the world of shipping, just like international traders have to deal with many charges, shippers also have their own expenses. One of these is the Bunker Adjustment Factor (BAF), an extra cost to cover the ups and downs of fuel prices. Depending on the deal between the shipper and carrier, BAF might be included in the freight charge or added separately.

Also called the Fuel Adjustment Factor, BAF considers how fuel prices change and the costs of running the ship. By taking these factors into account, BAF helps work out a more accurate shipping cost, making things clearer for both shippers and carriers in the complex world of shipping.

What is BAF?

BAF, or the Bunker Adjustment Factor, is a component of shipping costs calculated per twenty-foot equivalent unit (TEU), varying depending on the trade route. It reflects the fluctuating expenses attributed to fuel costs in shipping operations.

The start of the International Maritime Organization’s (IMO) 2020 regulations prompted the adoption of eco-friendly technologies to mitigate pollution from large container ships. Measures like the global sulfur cap, limiting sulfur emissions to 0.5% from the previous 3.5%, were introduced to address environmental concerns.

To comply with these regulations, shipping companies incur higher expenses, either through technology upgrades or cleaner fuel procurement. BAF is the mechanism through which these additional costs are passed on to shippers.

While the implementation of IMO regulations has stirred curiosity and raised questions within the shipping industry, BAF remains a critical aspect of shipping operations, reflecting the impact of regulatory changes on fuel-related costs.

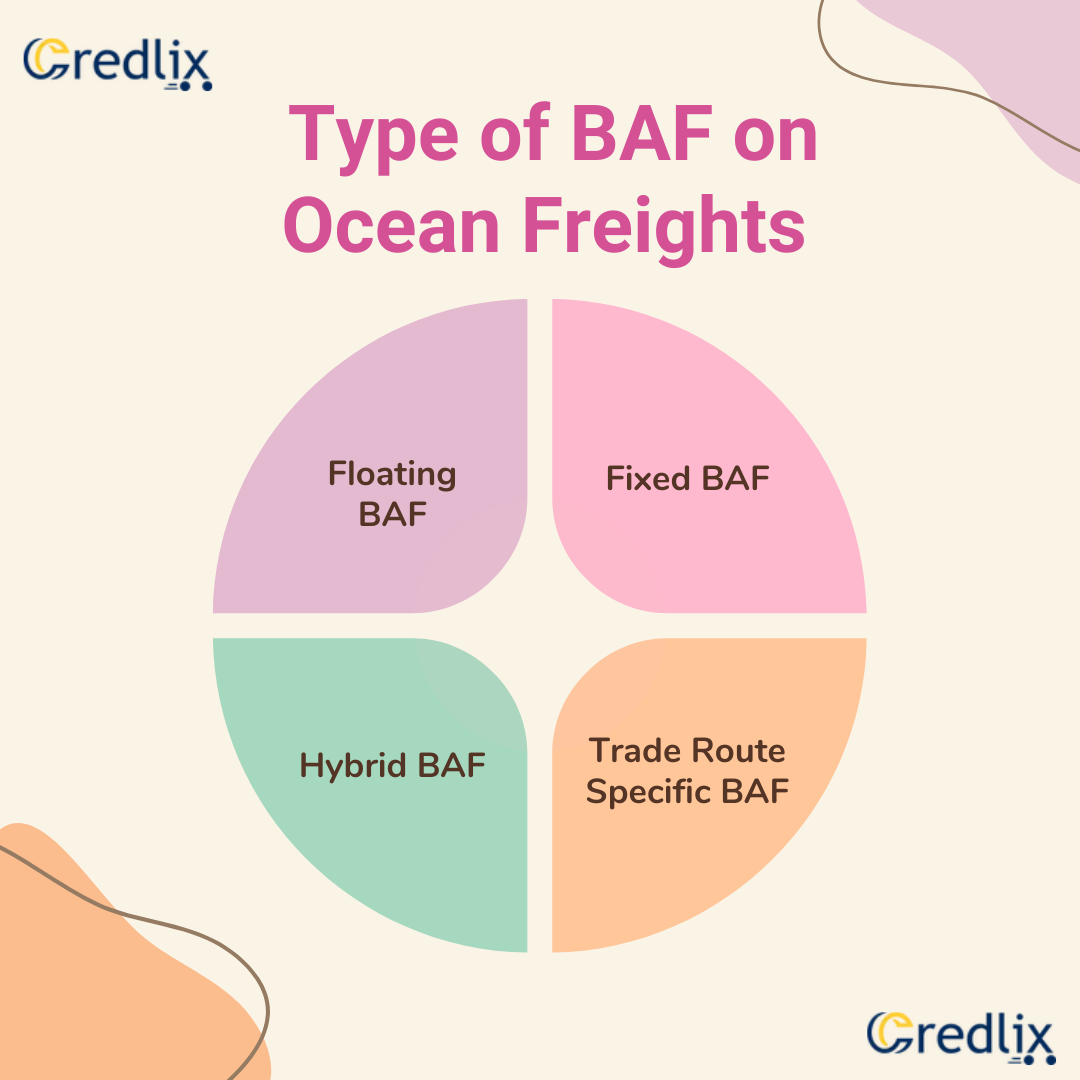

Type of BAF on Ocean Freights

Bunker Adjustment Factor (BAF) is a component of ocean freight charges that accounts for the fluctuating costs of fuel used by vessels. There are several types of BAF mechanisms used in the shipping industry, each with its own method of calculation and application. Let’s explore some common types:

Floating BAF

- Floating BAF is directly tied to the current market prices of fuel. This means that the BAF rate changes periodically in line with fluctuations in fuel prices.

- For example, if the market price of fuel increases, the BAF rate applied to a shipment will also increase. Conversely, if fuel prices decrease, the BAF rate will decrease accordingly.

- This type of BAF offers flexibility but can result in uncertainty for shippers as they may not know the exact BAF rate until closer to the shipment date.

Fixed BAF

- Fixed BAF, also known as a bunker surcharge, is a predetermined rate that remains constant for a specific period, regardless of changes in fuel prices.

- For instance, a shipping company may announce a fixed BAF rate for a quarter or a year, providing stability and predictability for shippers.

Fixed BAF rates are often based on average fuel prices over a certain period, allowing shipping lines to hedge against fuel price volatility.

Hybrid BAF

- Hybrid BAF combines elements of both floating and fixed BAF. It typically consists of a base rate that remains fixed for a set period, with adjustments made periodically based on changes in fuel prices.

- For example, a shipping line may set a fixed BAF rate for six months, with adjustments every month or quarter to account for fluctuations in fuel prices.

- Hybrid BAF offers a balance between stability and responsiveness to fuel price changes, providing some predictability while still reflecting market conditions.

Trade Route Specific BAF

- Some shipping lines apply BAF rates that vary depending on the specific trade route or geographic region.

- For instance, routes with longer distances or higher fuel consumption may have higher BAF rates compared to shorter routes.

- Trade route-specific BAF allows shipping lines to align BAF charges more closely with the actual fuel consumption and costs incurred on different routes.

Each type of BAF has its advantages and considerations for both shipping lines and shippers. Understanding the nuances of BAF mechanisms can help shippers anticipate and manage freight costs effectively in the dynamic environment of international shipping.

Who Issues the Bunker Adjustment Factor?

Bunker Adjustment Factor (BAF) rates are determined autonomously by individual shipping companies. However, the European Commission maintains vigilant oversight, closely monitoring these rates in relation to fuel prices to ensure fair and transparent pricing within the industry.

How to Calculate BAF?

Bunker Adjustment Factor (BAF) calculation in shipping is diverse, with each shipping line employing its unique formula, typically subject to monthly or bimonthly adjustments. To tackle concerns regarding transparency, many carriers have opted to disclose their calculation methodologies. For instance, Maersk Line, Limited, simplifies its BAF calculation using a formula that incorporates total fuel consumption, transit time, ship capacity, and a utilization factor.

Conversely, Hapag-Lloyd calculates BAF based on fuel price per tonne and fuel consumption relative to carried TEUs. Both approaches ensure flexibility and price security for carriers while addressing criticisms of opacity in BAF determination.

BAF = (Total fuel consumption x transit time) / (ship’s total capacity) x utilization factor

On the other hand, Hapag-Lloyd uses the following formula to calculate BAF:-

BAF = Fuel price per tonne x Fuel consumption in tonne/ Carried TEU

Note: Both these methods are based on flexible BAF and provide specific price security to the carriers.

The Impact of IMO 2020 on BAF and Shipping Operations

IMO 2020 signifies a landmark regulation aimed at mitigating global pollution by reducing emissions. Enacted on January 1, 2020, this directive mandates stringent controls on emissions through the compulsory implementation of the Data Collection System (DCS) by the International Maritime Organization (IMO).

In compliance, shipping lines globally are compelled to invest in technologies to minimize sulfur emissions, incurring additional costs. Consequently, shipping costs have surged either through logistical tariffs or the adoption of low-sulfur fuel, prompted by the necessity to adhere to the new regulations.

Furthermore, it’s necessary to adjust BAF charges to match the new fuel prices if shipping companies choose low-sulfur fuel. This means that IMO 2020 directly affects BAF rates worldwide, requiring changes to adapt to the changing rules.

Conclusion

The Bunker Adjustment Factor (BAF) is a crucial component in the realm of shipping, reflecting the dynamic nature of fuel costs and regulatory changes. The introduction of IMO 2020 has significantly impacted BAF rates globally, necessitating adjustments to align with the new regulations. Understanding BAF mechanisms and the influence of regulatory mandates is essential for navigating the complexities of international shipping operations effectively.

Also Read: LCL Shipments in Logistics and Shipping: Meaning, Costs, and More